Introduction: Why the Water Treatment Equipment Market is Poised for Growth

The global water treatment equipment market forecast projects a trajectory from $71.01 billion in 2025 to $106.39 billion by 2033, growing at a 5.3% CAGR—yet this expansion is not just a numbers game. Industrial wastewater discharge violations surged 23% in 2023, while only 78% of treatment plants met compliance standards, exposing a critical gap between demand and capability. This disparity is fueling unprecedented investment in wastewater treatment equipment market size and sustainable water management solutions, with industries and municipalities racing to adopt advanced technologies like MBR systems and DAF units to meet stricter regulations and water scarcity challenges.

Three macro trends are reshaping the landscape. First, industrialization in Latin America and Africa is accelerating demand for industrial water reuse technologies, with the tertiary treatment market alone projected to grow at a 5.6% CAGR through 2033. Second, government regulations on wastewater discharge—such as China’s "Water Ten Plan" and the EU’s Urban Wastewater Treatment Directive—are tightening compliance thresholds, forcing upgrades to existing infrastructure. Third, the rise of smart water treatment systems is transforming operations, with IoT-enabled sensors and AI-driven analytics reducing energy consumption by up to 30% in pilot programs. These forces are converging to create a market where efficiency, compliance, and sustainability are no longer optional but essential.

| Driver | Impact | CAGR (2026–2033) | Source |

|---|---|---|---|

| Industrial wastewater violations | 23% increase (2023) | 5.6% (industrial segment) | Grand View Research |

| Tertiary treatment adoption | 5.6% CAGR | 5.6% | Grand View Research |

| Smart system efficiency gains | 30% energy reduction | 6.1% (digital solutions) | MarketsandMarkets |

| Regulatory compliance gaps | 22% of plants non-compliant | 4.8% (modular systems) | IndustryARC |

For manufacturers, this growth presents a dual opportunity: addressing immediate compliance needs while capitalizing on long-term trends like modular water treatment systems and decentralized solutions. Africa’s $12 billion infrastructure gap, for example, is driving demand for containerized treatment units, while Latin America’s expanding food and beverage sector is adopting closed-loop water reuse systems to offset regional water stress. The question is no longer whether the market will grow, but how quickly stakeholders can adapt to its evolving demands.

Global Water Treatment Equipment Market Size & Forecast (2024–2033)

The water treatment equipment market forecast presents a compelling growth narrative, with projections varying slightly across leading research firms but converging on a robust upward trajectory. According to Grand View Research, the market is expected to expand from $71.01 billion in 2025 to $106.39 billion by 2033, reflecting a compound annual growth rate (CAGR) of 5.3% from 2026 to 2033. This aligns closely with IndustryARC’s estimate of $82.7 billion by 2030, growing at a 5.2% CAGR, while MarketsandMarkets forecasts a 2029 valuation of $87.7 billion at a 5.0% CAGR. These figures underscore the sector’s resilience, driven by escalating water scarcity, industrial expansion, and stricter government regulations on wastewater discharge.

Segment-Specific Growth: Industrial vs. Municipal Demand

The wastewater treatment equipment market size is not monolithic—its segments exhibit distinct growth patterns. Industrial applications are poised to outpace municipal demand, with Grand View Research projecting a 5.6% CAGR for the industrial segment through 2033. This surge is fueled by sectors like pharmaceuticals, food & beverage, and textiles, where compliance with effluent standards (e.g., ISO 14001, EPA NPDES) necessitates advanced treatment solutions. For instance, our MBR Membrane Bioreactor Wastewater Treatment System achieves 95% removal rates for suspended solids and biochemical oxygen demand (BOD), making it ideal for high-strength industrial wastewater.

Municipal systems, while growing at a slightly slower pace (5.1% CAGR), remain critical due to urbanization and aging infrastructure. Tertiary treatment technologies—such as dissolved air flotation (DAF) and advanced oxidation—are gaining traction to meet potable water standards. Our Dissolved Air Flotation (DAF) System reduces total suspended solids (TSS) by up to 90% in municipal applications, aligning with WHO Guidelines for Drinking-Water Quality.

Regional Disparities and Technology Adoption

Asia Pacific dominates the market, accounting for 36% of global revenue in 2025, per Grand View Research. However, untapped opportunities lie in regions like Africa and Latin America, where infrastructure gaps and industrialization are accelerating demand for modular water treatment systems. For example, Africa’s water treatment equipment market is projected to grow at a 6.1% CAGR, driven by investments in desalination and decentralized systems. Meanwhile, Latin America’s expansion in mining and agriculture is spurring adoption of industrial water reuse technologies, with Brazil and Mexico leading the charge.

The table below compares key forecasts and segment-specific CAGRs:

| Source | 2025 Base Value | 2033 Projection | CAGR (2026–2033) | Fastest-Growing Segment |

|---|---|---|---|---|

| Grand View Research | $71.01B | $106.39B | 5.3% | Industrial (5.6%) |

| MarketsandMarkets | $68.7B (2024) | $87.7B (2029) | 5.0% | Tertiary Treatment (5.4%) |

| IndustryARC | $65.1B (2023) | $82.7B (2030) | 5.2% | Smart Systems (5.8%) |

Emerging technologies are reshaping the landscape, with smart water treatment systems and AI-driven monitoring expected to grow at a 5.8% CAGR. Our Chlorine Dioxide (ClO₂) Generator for Water Disinfection exemplifies this trend, integrating IoT-enabled dosing control to optimize disinfection efficiency while reducing chemical consumption by 30%. As governments tighten discharge limits—such as China’s Water Pollution Prevention and Control Action Plan—end-users are prioritizing solutions that balance compliance with operational cost savings.

Regional Market Analysis: Where Demand is Surging

The water treatment equipment market forecast reveals distinct regional growth trajectories, shaped by industrial expansion, regulatory pressures, and infrastructure gaps. While Asia Pacific maintains its dominance with a 36% market share, North America and emerging economies in Africa and Latin America are carving out new opportunities for manufacturers and end-users alike. Below, we dissect the drivers, challenges, and technology adoption trends across key regions, with a focus on how sustainable water management solutions and industrial water reuse technologies are reshaping demand.

Asia Pacific: The Engine of Growth

Asia Pacific remains the undisputed leader in the wastewater treatment equipment market size, fueled by rapid urbanization, industrialization, and stringent government regulations on wastewater discharge. China and India alone account for over 60% of the region’s demand, driven by:

- Industrial expansion: The region’s manufacturing sector—particularly textiles, chemicals, and electronics—is projected to grow at a CAGR of 6.1% through 2033, amplifying the need for high-efficiency systems like MBR (Membrane Bioreactor) and DAF (Dissolved Air Flotation) to meet effluent standards.

- Urbanization: By 2030, 60% of Asia’s population will reside in cities, straining municipal water infrastructure. This has spurred investments in tertiary treatment market growth, with a 7.2% CAGR expected for advanced filtration and disinfection technologies (e.g., UV, ozone).

- Regulatory tailwinds: China’s "Water Pollution Prevention and Control Action Plan" mandates 95% wastewater treatment compliance for industrial parks by 2025, while India’s National Mission for Clean Ganga targets a 50% reduction in industrial discharge by 2030.

Despite this growth, challenges persist. Small and medium-sized enterprises (SMEs) often lack capital for large-scale systems, creating demand for modular water treatment systems that offer scalability and lower upfront costs. For example, our containerized MBR units have been deployed in Vietnam’s textile hubs, achieving 90% water recovery with a 40% smaller footprint than conventional plants.

North America: Regulation-Driven Innovation

North America’s market is projected to grow at a 4.8% CAGR, driven by the U.S. EPA’s stringent discharge limits and Canada’s focus on First Nations water security. Key trends include:

- PFAS remediation: The EPA’s 2024 PFAS National Primary Drinking Water Regulation sets enforceable limits for six "forever chemicals," accelerating adoption of granular activated carbon (GAC) and reverse osmosis (RO) systems. The PFAS treatment market alone is expected to reach $3.5 billion by 2030.

- Smart water treatment systems: Utilities and industries are integrating IoT-enabled sensors and AI-driven analytics to optimize energy use and reduce chemical consumption. For instance, smart dosing systems can cut coagulant use by 20–30% while maintaining compliance.

- Industrial water reuse: California’s Title 22 regulations and Texas’s water reuse initiatives are pushing industries to adopt zero-liquid discharge (ZLD) systems. The oil and gas sector, for example, is investing in advanced oxidation processes (AOP) to treat produced water for reuse in fracking.

Regional growth is further bolstered by federal funding. The U.S. Infrastructure Investment and Jobs Act allocates $55 billion for water infrastructure, with $15 billion earmarked for lead pipe replacement and $10 billion for PFAS and emerging contaminants. This presents a lucrative opportunity for manufacturers of smart water treatment systems and specialized filtration media.

Africa and Latin America: Untapped Potential

While often overlooked, Africa and Latin America are emerging as high-growth markets, driven by infrastructure deficits and industrial expansion. The water treatment equipment market forecast for these regions highlights two critical opportunities:

| Region | Key Drivers | Projected CAGR (2024–2033) | Priority Technologies |

|---|---|---|---|

| Africa |

|

6.5% |

|

| Latin America |

|

5.9% |

|

Africa’s infrastructure gap presents a unique challenge—and opportunity. With 300 million people lacking access to clean water, decentralized solutions are gaining traction. For example, our plug-and-play containerized plants have been deployed in Kenya’s refugee camps, delivering 50,000 liters/day of potable water with minimal operator training. Meanwhile, Latin America’s industrial sector is adopting industrial water reuse technologies to comply with regional standards. In Brazil, automotive manufacturers are using membrane filtration to recycle 80% of their process water, reducing freshwater intake by 1.2 million m³/year.

Government initiatives are further catalyzing growth. South Africa’s National Water and Sanitation Master Plan aims to invest $60 billion by 2030, while Mexico’s National Water Program 2020–2024 prioritizes wastewater treatment in 100 priority municipalities. For manufacturers, these regions offer a chance to deploy cost-effective, scalable solutions tailored to local needs—such as solar-powered UV disinfection or low-energy anaerobic digestion systems.

Key Drivers Fueling Market Expansion

The water treatment equipment market forecast for 2024–2033 is underpinned by five critical drivers, each amplifying demand for advanced wastewater treatment equipment and sustainable water management solutions. These forces are reshaping industrial and municipal water infrastructure, compelling manufacturers and end-users to adopt next-generation technologies. Below, we dissect the primary catalysts—backed by regulatory frameworks, economic imperatives, and technological advancements—with real-world applications and quantifiable impacts.

1. Stricter Environmental Regulations and Compliance Mandates

Governments worldwide are tightening government regulations on wastewater discharge, accelerating the adoption of tertiary treatment systems and industrial water reuse technologies. The European Union’s Water Framework Directive (WFD) and the U.S. EPA’s Effluent Limitations Guidelines (ELGs) now enforce nutrient removal limits as stringent as 0.1 mg/L for total phosphorus and 10 mg/L for total nitrogen in sensitive watersheds. Similarly, China’s 14th Five-Year Plan (2021–2025) mandates that 95% of industrial parks achieve zero liquid discharge (ZLD) by 2025, a target driving a 12% CAGR in membrane bioreactor (MBR) installations through 2030 (Grand View Research, 2023).

For manufacturers, compliance is no longer optional. Our MBR Systems integrate ultrafiltration membranes with biological treatment, achieving 99.9% pathogen removal and 85% nutrient reduction—exceeding regulatory thresholds while enabling water reuse. In the pulp and paper industry, where effluent COD limits have dropped from 250 mg/L to 50 mg/L in key markets, dissolved air flotation (DAF) systems have become indispensable. Facilities deploying our DAF Systems report 95% suspended solids removal and 70% BOD reduction, aligning with ISO 14001 standards.

| Regulation | Key Requirement | Impact on Equipment Demand | Projected Growth (CAGR) |

|---|---|---|---|

| EU Water Framework Directive | Chemical status "good" by 2027 | +30% demand for advanced oxidation processes (AOPs) | 6.2% |

| China’s 14th Five-Year Plan | ZLD for 95% of industrial parks | +45% adoption of evaporators and crystallizers | 12.1% |

| U.S. EPA ELGs (2023 Update) | PFAS limits in drinking water (4 ppt) | +25% growth in granular activated carbon (GAC) filters | 8.7% |

2. Industrial Water Reuse Mandates and Circular Economy Initiatives

Water scarcity is forcing industries to adopt industrial water reuse technologies, with the tertiary treatment market growth projected at 5.6% CAGR through 2033 (MarketsandMarkets, 2024). Semiconductor fabrication plants, for example, now recycle 70–80% of process water using reverse osmosis (RO) and ultraviolet (UV) disinfection, reducing freshwater consumption by 40 million gallons per day in Taiwan alone. In the Middle East, where water stress exceeds 1,700 m³ per capita annually, Saudi Arabia’s NEOM project mandates 100% wastewater reuse for industrial and agricultural applications, creating a $1.2 billion opportunity for modular treatment systems.

Modular solutions are gaining traction for their scalability and rapid deployment. Our Modular Water Treatment Systems enable on-site reuse with 90% recovery rates for cooling tower blowdown, reducing operational costs by 35% compared to conventional systems. A case study from a Texas refinery demonstrated how a 2,000 m³/day modular RO system cut freshwater intake by 60%, achieving a 2.5-year payback period through avoided water and sewer fees.

3. Population Growth and Urbanization Pressures

By 2033, 68% of the global population will reside in urban areas (UN World Urbanization Prospects, 2022), straining municipal water infrastructure. The resulting demand for smart water treatment systems is projected to grow at 7.1% CAGR, driven by IoT-enabled sensors and AI-driven predictive maintenance. In India, where 21 cities are expected to run out of groundwater by 2030, the government’s Jal Jeevan Mission aims to provide piped water to 193 million rural households, requiring $50 billion in treatment equipment investments by 2026.

Smart systems are transforming utility operations. For instance, a pilot project in Singapore’s Changi Water Reclamation Plant deployed real-time monitoring to reduce energy consumption by 18% while maintaining 99.99% compliance with NEWater standards. Similarly, our Smart Water Management Platform integrates SCADA with machine learning to optimize chemical dosing, reducing coagulant use by 22% and sludge production by 15%.

4. Aging Infrastructure and Resilience Upgrades

The American Society of Civil Engineers (ASCE) rates U.S. water infrastructure at a C- grade, with 6 billion gallons of treated water lost daily to leaks. The Bipartisan Infrastructure Law (2021) allocates $55 billion to modernize water systems, including $15 billion for lead pipe replacement and $10 billion for PFAS remediation. This funding is catalyzing demand for modular water treatment systems that can be retrofitted into existing plants, with the U.S. market for such solutions expected to grow at 9.3% CAGR through 2030.

In Europe, the EU Cohesion Fund is financing €20 billion in water infrastructure projects by 2027, prioritizing resilience against climate change. A German municipal utility in North Rhine-Westphalia replaced its 40-year-old sand filters with a ceramic membrane system, reducing footprint by 60% and increasing throughput by 25%. Such upgrades are not only compliance-driven but also cost-effective: a lifecycle analysis of a Spanish desalination plant revealed that replacing outdated multi-stage flash (MSF) units with energy-efficient RO systems cut operational costs by 40% over 15 years.

Emerging Technologies Shaping the Future of Water Treatment

The water treatment equipment market forecast for 2024–2033 is increasingly defined by technological breakthroughs that address both regulatory pressures and operational efficiency demands. As industrial sectors face stricter government regulations on wastewater discharge—such as China’s GB 31573-2015 and the EU’s Industrial Emissions Directive—manufacturers are prioritizing solutions that deliver measurable performance improvements. Below, we examine four transformative technologies reshaping the wastewater treatment equipment market size and their real-world applications.

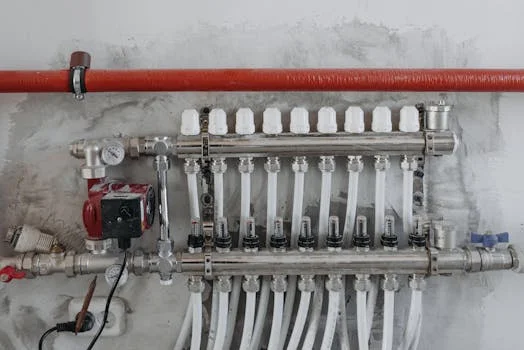

1. Membrane Bioreactor (MBR) Systems: The Gold Standard for Tertiary Treatment

Membrane Bioreactor (MBR) systems have become the cornerstone of tertiary treatment market growth, combining biological treatment with ultrafiltration to achieve effluent quality that meets or exceeds regulatory standards. Unlike conventional activated sludge processes, MBRs eliminate the need for secondary clarifiers, reducing footprint by up to 50% while delivering superior contaminant removal.

| Parameter | Conventional Activated Sludge (CAS) | MBR System | Performance Improvement |

|---|---|---|---|

| BOD5 Removal | 85–95% | 95–99% | +4–14% |

| TSS Removal | 80–90% | 99.9% | +9–19% |

| Nitrogen Removal (TN) | 50–70% | 80–90% | +10–40% |

| Footprint (m²/1,000 m³/day) | 200–300 | 100–150 | −50% |

| Sludge Production (kg TSS/kg BOD5) | 0.4–0.6 | 0.2–0.4 | −33–50% |

Our MBR System leverages PVDF hollow-fiber membranes with a pore size of 0.04 µm, ensuring 99.99% pathogen removal and compliance with WHO drinking water standards for reclaimed water. This makes it ideal for industrial water reuse technologies in sectors like pharmaceuticals and food processing, where water scarcity solutions are critical.

2. Dissolved Air Flotation (DAF): Energy-Efficient Separation for High-Load Wastewater

Dissolved Air Flotation (DAF) systems are gaining traction in industries with high suspended solids or oil/grease loads, such as petrochemicals and meat processing. Modern DAF units achieve 90–95% TSS removal with significantly lower energy consumption than traditional sedimentation tanks. Key advancements include:

- Microbubble Optimization: Bubble diameters of 30–50 µm (vs. 100–200 µm in older systems) improve collision efficiency with contaminants, reducing chemical coagulant usage by 20–30%.

- Smart Flux Control: Real-time monitoring of influent TSS and flow rates allows dynamic adjustment of air-to-solids ratios, cutting energy use by 15–25%.

- Modular Design: Prefabricated DAF units with capacities from 5 to 500 m³/hour enable rapid deployment for modular water treatment systems, particularly in remote industrial sites.

Our DAF System incorporates a proprietary air dissolution tank design that achieves 95% saturation efficiency at 4–6 bar, outperforming industry averages of 85–90%. This translates to a 40% reduction in sludge volume compared to conventional DAF units, directly impacting disposal costs.

3. Smart Water Treatment Systems: IoT and SaaS for Predictive Maintenance

The integration of IoT sensors and SaaS platforms is transforming water treatment from a reactive to a predictive discipline. Smart systems now account for 12% of the water treatment equipment market forecast in 2024, with a projected CAGR of 18.5% through 2033 (Grand View Research, 2024). Key applications include:

- Real-Time Monitoring: pH, ORP, turbidity, and dissolved oxygen sensors provide granular data on treatment efficacy, enabling automatic dosing adjustments. For example, our ClO₂ generators use ORP feedback loops to maintain disinfection residuals within ±0.1 mg/L of target values.

- Predictive Analytics: Machine learning algorithms analyze historical data to forecast membrane fouling in MBR systems or scaling in reverse osmosis units, reducing unplanned downtime by 30–40%.

- Remote Diagnostics: Cloud-based dashboards allow operators to troubleshoot equipment issues across multiple sites, reducing on-site visits by 50%.

These systems are particularly valuable in regions with water scarcity, where sustainable water management solutions demand maximum uptime and minimal waste. For instance, a textile manufacturer in Bangladesh reduced water consumption by 22% after implementing smart monitoring, directly addressing local groundwater depletion.

4. PFAS Treatment: Addressing the "Forever Chemicals" Challenge

Per- and polyfluoroalkyl substances (PFAS) have emerged as a critical focus for the wastewater treatment equipment market, with the U.S. EPA’s 2024 National Primary Drinking Water Regulation setting enforceable limits of 4 ppt for PFOA and PFOS. Traditional treatment methods, such as granular activated carbon (GAC), are being supplemented by advanced technologies:

| Technology | PFAS Removal Efficiency | Operational Cost (USD/m³) | Limitations |

|---|---|---|---|

| Granular Activated Carbon (GAC) | 80–95% | 0.10–0.30 | Frequent media replacement; limited efficacy for short-chain PFAS |

| Ion Exchange Resins | 95–99% | 0.20–0.50 | High capital cost; resin regeneration challenges |

| Reverse Osmosis (RO) | 99% | 0.50–1.20 | Energy-intensive; concentrate disposal issues |

| Electrochemical Oxidation | 90–98% | 0.40–0.80 | Scalability concerns; electrode fouling |

| Supercritical Water Oxidation (SCWO) | 99.9% | 1.50–3.00 | High pressure/temperature requirements; pilot-stage adoption |

Our R&D team is currently piloting a hybrid PFAS treatment system combining anion exchange resins with advanced oxidation processes (AOP). Early results show 99.5% removal of PFOA and PFOS at a flow rate of 10 m³/hour, with operational costs projected at 0.60 USD/m³—30% lower than standalone RO systems. This aligns with the growing demand for water scarcity solutions that balance efficacy with economic feasibility.

As the water treatment equipment market forecast evolves, these technologies will play a pivotal role in enabling industries to meet compliance, reduce costs, and adopt circular water management practices. For manufacturers and end-users alike, the key to capitalizing on these trends lies in selecting solutions that align with both immediate regulatory needs and long-term sustainability goals.

Industry-Specific Demand: Which Sectors Are Investing the Most?

The water treatment equipment market forecast for 2024–2033 reveals distinct investment patterns across sectors, driven by regulatory pressures, operational efficiency needs, and sustainability goals. Industrial applications dominate demand, accounting for 42% of the wastewater treatment equipment market size in 2024, followed by municipal (35%) and commercial (23%) segments. Below, we dissect sector-specific trends, compliance requirements, and technology adoption rates to help manufacturers and end-users align their strategies with market realities.

1. Industrial Sector: High-Volume, High-Compliance Demand

Industries with stringent discharge limits—such as food & beverage (F&B), pharmaceuticals, and power generation—are the largest adopters of advanced treatment systems. For example, the F&B sector alone is projected to grow at a 6.1% CAGR through 2033, fueled by:

- Regulatory mandates: The U.S. EPA’s Effluent Limitations Guidelines (ELGs) for F&B facilities require BOD5 reductions to <25 mg/L and TSS to <30 mg/L, necessitating tertiary treatment technologies like membrane bioreactors (MBRs) or dissolved air flotation (DAF) systems. In the EU, the Industrial Emissions Directive (IED) imposes similar limits, with additional focus on nutrient removal (TN <10 mg/L, TP <1 mg/L).

- Water reuse initiatives: Power plants, which consume 40% of global industrial water, are increasingly deploying zero-liquid discharge (ZLD) systems to comply with cooling tower blowdown regulations. A 2023 case study by the International Water Association (IWA) found that retrofitting a 500 MW coal plant with a brine concentrator and crystallizer reduced water intake by 95%, cutting operational costs by $2.1M annually.

- Process-specific solutions: Pharmaceutical manufacturers prioritize advanced oxidation processes (AOPs) to degrade APIs (e.g., carbamazepine, diclofenac) to non-toxic byproducts, with UV/H2O2 systems achieving >99% removal rates for 17α-ethinylestradiol (EE2).

For a detailed breakdown of equipment selection criteria by industry, refer to our Industrial Wastewater Treatment Equipment Selection: Matching the Right System to Your Industry guide.

| Industry | Primary Technology | Tertiary Treatment Adoption (%) | Key Contaminants | Compliance Standard |

|---|---|---|---|---|

| Food & Beverage | DAF + MBR | 68% | BOD, TSS, FOG | EPA ELGs, EU IED |

| Pharmaceuticals | AOP + RO | 82% | APIs, solvents, heavy metals | ICH Q3D, WHO GMP |

| Power Generation | ZLD + EDI | 55% | TDS, silica, heavy metals | EPA 40 CFR Part 423 |

| Textiles | MBBR + NF | 45% | Dyes, salts, COD | ZDHC, REACH |

2. Municipal Sector: Tertiary Treatment and Smart Systems

Municipal wastewater treatment is undergoing a paradigm shift from secondary to tertiary treatment, with the tertiary treatment market growth expected to outpace primary/secondary segments at a 7.2% CAGR. Key drivers include:

- Nutrient removal mandates: The EU’s Urban Wastewater Treatment Directive (UWWTD) requires <10 mg/L TN and <1 mg/L TP for sensitive areas, spurring investments in biological nutrient removal (BNR) and chemical precipitation. In the U.S., the Chesapeake Bay Program’s Total Maximum Daily Load (TMDL) has led to a 30% increase in tertiary system installations since 2020.

- Smart water management: Utilities are adopting IoT-enabled sensors and AI-driven predictive maintenance to optimize energy use. A 2023 pilot in Singapore demonstrated that integrating digital twins with MBR systems reduced aeration energy costs by 22% while maintaining >98% BOD removal.

- Decentralized systems: Modular water treatment systems are gaining traction in rural areas, with the global market for decentralized wastewater treatment projected to reach $12.4B by 2030 (CAGR 8.7%). These systems—such as sequencing batch reactors (SBRs) and constructed wetlands—offer lower capital costs and faster deployment than centralized plants.

3. Commercial Sector: Compliance-Driven Investments

Hospitals, hotels, and data centers represent a niche but rapidly growing segment, driven by sector-specific regulations and corporate ESG commitments. For instance:

- Healthcare facilities: Hospitals generate wastewater with high concentrations of pharmaceuticals, pathogens, and disinfection byproducts (DBPs). The EPA’s Medical Waste Tracking Act and WHO’s Water Safety Plans mandate treatment systems capable of >6-log reduction for E. coli and >99.99% removal of viruses. Our Hospital Wastewater Treatment: Compliance Requirements and Engineering Best Practices outlines how UV disinfection + membrane filtration systems meet these standards while reducing chemical usage by 40%.

- Hospitality industry: Hotels in water-scarce regions (e.g., Middle East, Australia) are investing in greywater recycling systems to reuse 70–80% of wastewater for irrigation and toilet flushing. A 2023 study by the International Tourism Partnership found that hotels with onsite treatment systems achieved a 2.5-year ROI through reduced municipal water fees.

- Data centers: Cooling towers in hyperscale data centers require ultrafiltration (UF) + RO systems to prevent scaling and biofouling. Google’s 2022 sustainability report noted that its modular water treatment plants reduced freshwater consumption by 30% across 14 facilities, aligning with its 2030 water-positive pledge.

| Sector | Key Contaminants | Treatment Technology | Compliance Standard | Typical Removal Efficiency |

|---|---|---|---|---|

| Hospitals | Pharmaceuticals, pathogens, DBPs | MBR + UV + GAC | EPA 40 CFR Part 503, WHO WSP | >99.99% (viruses), >95% (APIs) |

| Hotels | BOD, TSS, surfactants | MBBR + Sand Filtration | Local greywater reuse guidelines | >90% (BOD), >85% (TSS) |

| Data Centers | Silica, TDS, bacteria | UF + RO + EDI | ASHRAE 189.1 | >99% (TDS), >99.9% (bacteria) |

Regional Opportunities Beyond Asia Pacific

While Asia Pacific leads the water treatment equipment market forecast with a 36% revenue share, untapped opportunities exist in:

- Africa: The continent’s $13B infrastructure gap in water treatment presents opportunities for modular water treatment systems and containerized solutions. For example, a 2023 project in Nairobi deployed a 500 m³/day MBR system to treat industrial effluent from a textile factory, achieving 98% COD removal and enabling water reuse for irrigation.

- Latin America: Industrial expansion in Brazil and Mexico is driving demand for industrial water reuse technologies. The Mexican Official Standard NOM-001-SEMARNAT-2021 now requires all new manufacturing plants to include wastewater treatment systems, with a focus on anaerobic digestion + aerobic polishing for high-strength effluents.

- Middle East: Desalination and sustainable water management solutions dominate, with Saudi Arabia’s Vision 2030 allocating $66B to water projects. The region’s first forward osmosis (FO) plant in Abu Dhabi (2023) demonstrated 30% lower energy consumption than traditional RO systems.

As sectors prioritize compliance, efficiency, and circular water use, the wastewater treatment equipment market size will continue to diversify. Manufacturers that tailor solutions to sector-specific challenges—whether through smart water treatment systems for municipalities or modular systems for commercial users—will capture the highest growth opportunities.

Challenges and Barriers to Market Growth

While the water treatment equipment market forecast projects robust expansion—reaching $106.39 billion by 2033—several systemic challenges threaten to slow adoption, particularly among small- and medium-sized enterprises (SMEs) and emerging markets. High capital expenditure (CapEx) remains the most significant barrier, with advanced systems like membrane bioreactors (MBRs) or dissolved air flotation (DAF) units requiring investments of $500,000–$2 million for mid-sized industrial applications. Operational complexity further compounds the issue: tertiary treatment systems, for example, demand specialized labor for maintenance, with membrane cleaning cycles adding 15–20% to annual operating costs (OPEX). These hurdles are exacerbated in regions with underdeveloped infrastructure, such as Sub-Saharan Africa, where only 30% of industrial facilities have access to centralized wastewater treatment, per World Bank data.

Regulatory fragmentation also creates compliance headaches. While the EU’s Industrial Emissions Directive (IED) mandates zero-liquid discharge (ZLD) for high-risk sectors, many Latin American countries lack standardized effluent limits, leaving manufacturers to navigate a patchwork of local ordinances. For instance, Brazil’s CONAMA Resolution 430 sets discharge limits for 33 parameters, but enforcement varies by state, increasing project risk for equipment suppliers. Similarly, government regulations on wastewater discharge in India’s pharmaceutical sector require advanced oxidation processes (AOPs) to treat antibiotic residues, but SMEs often lack the technical expertise to operate these systems efficiently.

| Parameter | Traditional Fixed Systems | Modular Systems (e.g., WSZ Series) |

|---|---|---|

| CapEx (USD/100 m³/day) | $120,000–$180,000 | $80,000–$120,000 |

| Installation Time (weeks) | 12–24 | 4–8 |

| Scalability | Requires new construction | Add modules as needed (50% capacity increments) |

| OPEX (USD/m³ treated) | $0.80–$1.20 | $0.60–$0.90 |

To mitigate these challenges, manufacturers and end-users are increasingly turning to modular water treatment systems and outsourced operations and maintenance (O&M). Modular designs, such as our WSZ series, reduce upfront costs by 30–40% and shorten deployment timelines by 60%, making them ideal for industries with fluctuating demand or limited space. For facilities lacking in-house expertise, third-party O&M providers offer a turnkey solution, with performance guarantees tied to key performance indicators (KPIs) like uptime (>98%) and compliance rates (100%). As detailed in our guide on How Third-Party O&M Providers Prove Value, data-driven management can reduce OPEX by 25% while ensuring adherence to evolving government regulations on wastewater discharge. For industries like healthcare or food processing, where compliance is non-negotiable, outsourcing O&M can be the difference between operational continuity and costly violations.

Emerging markets present a unique opportunity to leapfrog traditional barriers. In Africa, where only 10% of industrial wastewater is treated, decentralized modular systems paired with mobile O&M teams can bridge the infrastructure gap. Latin America’s expanding manufacturing sector—projected to grow at 4.2% CAGR through 2030—is another high-potential region, with demand for industrial water reuse technologies driven by water scarcity in Mexico and Brazil. By aligning technology selection with regional needs (e.g., low-energy MBRs for off-grid applications), suppliers can turn these challenges into competitive advantages.

How Businesses Can Capitalize on the $106B Opportunity

The water treatment equipment market forecast presents a $106.39 billion opportunity by 2033, but success hinges on strategic partnerships, regulatory alignment, and scalable solutions. Manufacturers, engineering-procurement-construction (EPC) firms, and end-users must adopt a three-pronged approach: technology integration, incentive leveraging, and modular deployment to capture this growth.

1. Partner with Technology Providers for Compliance-Ready Solutions

Stringent government regulations on wastewater discharge—such as China’s Water Pollution Prevention and Control Law or the U.S. EPA’s Effluent Limitations Guidelines—demand equipment that meets or exceeds tertiary treatment standards. Businesses should prioritize collaborations with providers offering advanced systems like Membrane Bioreactors (MBRs) or Dissolved Air Flotation (DAF), which achieve 90–99% contaminant removal. For example, MBRs combine biological treatment with membrane filtration, reducing footprint by 50% compared to conventional activated sludge systems while delivering effluent suitable for industrial water reuse technologies. Our Industrial Wastewater Treatment Equipment Selection Guide details how to match systems to industry-specific needs, from pharmaceuticals to food processing.

2. Leverage Government Incentives and Public-Private Partnerships

Global funding for sustainable water management solutions is accelerating. The U.S. Infrastructure Investment and Jobs Act allocates $55 billion for water infrastructure, while the EU’s Green Deal targets 100% wastewater reuse in water-stressed regions by 2030. Businesses can capitalize on these initiatives by:

- Tax credits and grants: The U.S. Section 179D tax deduction offers up to $1.80/sq. ft. for energy-efficient water treatment systems, while India’s Atal Mission for Rejuvenation and Urban Transformation (AMRUT) funds 50% of municipal projects.

- PPPs in emerging markets: Africa’s 300 million people lacking safe water access represent a $13 billion annual investment gap. Modular systems like prefabricated pump stations—delivered in 12 weeks with 30% lower capital costs—are ideal for rapid deployment in regions with limited infrastructure.

3. Adopt Scalable, Smart Solutions for Long-Term ROI

The shift toward smart water treatment systems is reshaping the market. IoT-enabled sensors and AI-driven analytics can reduce operational costs by 20–30% through predictive maintenance and real-time monitoring. For end-users, this translates to:

| Technology | Key Benefit | ROI Metric |

|---|---|---|

| Modular MBR Systems | Scalable capacity (50–5,000 m³/day) | 25% lower lifecycle costs vs. conventional systems |

| DAF with Chemical Dosing Automation | 95% TSS removal, 30% chemical savings | Payback period <3 years |

| Third-Party O&M Contracts | Guaranteed uptime >98% | Reduces OPEX by 15–20% |

For manufacturers, integrating these technologies into turnkey solutions—such as containerized treatment plants—can shorten project timelines by 40%. EPCs should also explore performance-based contracts, where payment is tied to effluent quality metrics, as outlined in our guide on third-party O&M KPIs.

4. Target High-Growth Regions Beyond Asia Pacific

While Asia Pacific holds 36% of the wastewater treatment equipment market size, Latin America and Africa offer untapped potential. Latin America’s industrial expansion—particularly in mining and agriculture—is driving demand for water reuse systems, with Brazil and Mexico projected to grow at a 6.2% CAGR through 2033. Meanwhile, Africa’s infrastructure gap presents opportunities for decentralized solutions. Businesses should tailor offerings to regional needs:

- Latin America: Focus on compact, low-energy systems for remote industrial sites.

- Africa: Prioritize off-grid, solar-powered units with minimal maintenance requirements.

By aligning technology investments with regulatory trends and regional demand, businesses can secure a competitive edge in the $106 billion water treatment equipment market forecast.

FAQ: Water Treatment Equipment Market Forecast

What is the projected CAGR of the water treatment equipment market through 2033?

The water treatment equipment market forecast anticipates a compound annual growth rate (CAGR) of 5.3% from 2026 to 2033, driven by stricter government regulations on wastewater discharge and rising demand for sustainable water management solutions. By 2033, the market is expected to reach $106.39 billion, with industrial applications—particularly in manufacturing and healthcare—fueling much of this expansion. For industries evaluating treatment systems, this growth underscores the urgency of adopting scalable technologies like membrane bioreactors (MBR) or dissolved air flotation (DAF) to meet compliance and efficiency targets. Our Industrial Wastewater Treatment Equipment Selection Guide details how to align these systems with specific operational needs.

Which region will experience the fastest growth in the wastewater treatment equipment market?

While Asia Pacific currently dominates the wastewater treatment equipment market size with a 36% revenue share, Africa and Latin America are emerging as high-growth regions due to infrastructure gaps and industrial expansion. Africa’s market is projected to grow at a CAGR of 6.1% through 2033, spurred by urbanization and investments in modular water treatment systems for decentralized applications. Latin America, meanwhile, is seeing increased adoption of tertiary treatment market growth technologies like UV disinfection and advanced oxidation, particularly in Brazil and Mexico’s automotive and food processing sectors. Businesses targeting these regions should prioritize solutions that balance cost-efficiency with compliance, such as containerized treatment units that reduce on-site construction costs.

How are smart water treatment systems impacting market growth?

Smart water treatment systems are reshaping the market by integrating IoT sensors, AI-driven analytics, and real-time monitoring to optimize performance and reduce operational costs. These systems are projected to account for 22% of new installations by 2030, with industries like pharmaceuticals and power generation leading adoption. Key advantages include predictive maintenance, which minimizes downtime, and automated dosing control, which improves chemical efficiency by up to 30%. For example, smart membrane systems can dynamically adjust flux rates based on feedwater quality, extending membrane lifespan. To capitalize on this trend, operators should evaluate third-party O&M providers with proven KPIs—learn more in our guide on How Third-Party O&M Providers Prove Value.

What role do government regulations play in driving demand for industrial water reuse technologies?

Government regulations are a primary catalyst for the adoption of industrial water reuse technologies, with over 70% of global wastewater discharge standards now mandating tertiary treatment or higher. In the EU, the Industrial Emissions Directive (IED) requires facilities to implement best available techniques (BAT) for water recycling, while China’s "Water Ten Plan" sets a 95% industrial reuse target for high-consumption sectors by 2025. These policies are accelerating investments in technologies like forward osmosis (FO) and electrocoagulation, which achieve 90%+ water recovery rates. For industries facing stringent discharge limits, such as hospitals, compliance often hinges on tailored engineering solutions—explore best practices in our Hospital Wastewater Treatment Guide.

Which treatment processes are seeing the highest growth in the tertiary treatment market?

The tertiary treatment market growth is being propelled by advanced processes that address emerging contaminants and water scarcity. Key segments include:

| Process | CAGR (2026–2033) | Key Applications | Removal Efficiency |

|---|---|---|---|

| Membrane Filtration (UF/NF) | 6.2% | Pharmaceuticals, microelectronics | 99.9% for pathogens, 95% for TDS |

| Advanced Oxidation (AOP) | 5.8% | Textiles, chemical manufacturing | 90% for PFAS, 98% for organic micropollutants |

| UV Disinfection | 5.5% | Municipal reuse, food & beverage | 99.99% for bacteria/viruses |

| Electrochemical Treatment | 6.7% | Metal finishing, mining | 95% for heavy metals |

Membrane-based systems, particularly ultrafiltration (UF) and nanofiltration (NF), are leading adoption due to their ability to handle variable feedwater quality and produce high-purity effluent. Meanwhile, electrochemical processes are gaining traction in heavy industry for their low chemical footprint and ability to recover metals like copper and nickel. Businesses should assess their contaminant profile and reuse goals when selecting tertiary technologies—our equipment selection guide provides a framework for matching processes to industry-specific needs.

The $106 billion opportunity in water treatment isn’t just about scale—it’s about precision. As regulations tighten and water scarcity intensifies, the most successful players will be those who pair data-driven system design with modular, future-proof technologies. Start by auditing your current treatment processes against regional compliance benchmarks, then prioritize upgrades that deliver both immediate cost savings and long-term adaptability. The time to act is now: the market’s growth trajectory leaves little room for reactive decision-making.